The Agentic Economy

Why we think the fintech crowd is building on the wrong substrate

Every major payments company has shipped an “agentic” product in the past two months. Stripe and OpenAI launched the Agentic Commerce Protocol. Google and Shopify launched the Universal Commerce Protocol. Visa announced Agentic Ready. Mastercard backed the FIDO Alliance on agentic standards and quietly paid $1.8B for BVNK to own stablecoin infrastructure. AmEx shipped the Agentic Commerce Experiences Developer Kit. PayPal reorganized around an AI transformation and declared it was “becoming a tech company again.”

The new capabilities are real but narrow. Each product gives agents virtual credentials, spending limits, and merchant whitelists. The agent transacts without asking the human to approve each charge. What did not change is the underlying model. Authorization still flows from humans. Chargebacks still require humans to dispute. KYC still binds to human identity. Liability still lands on humans.

The agent looks like a principal, but it is still a delegate.

That works fine for the first wave of agentic commerce, where a human tells an agent to book flights or order groceries. But it doesn’t work for what comes next: agents transacting with other agents, services pricing themselves dynamically per call, software paying software for compute, data, and bandwidth.

Stablecoins are the only payment substrate ever built for non-human counterparties. They are programmable. They settle in seconds with no chargeback infrastructure. An agent can hold a balance, spend it, and transact at any size, including amounts that make no sense on credit card rails. There is no consent loop because consent was never the model.

Even the incumbents are betting on stablecoins: Stripe acquired Bridge for $1.1B, Mastercard bought BVNK for $1.8B, and the Machine Payments Protocol Stripe built with Tempo routes payments natively to stablecoins.

Most of the venture money flowing into the category right now is going to the wrong layer. To see why, it helps to disaggregate the problem.

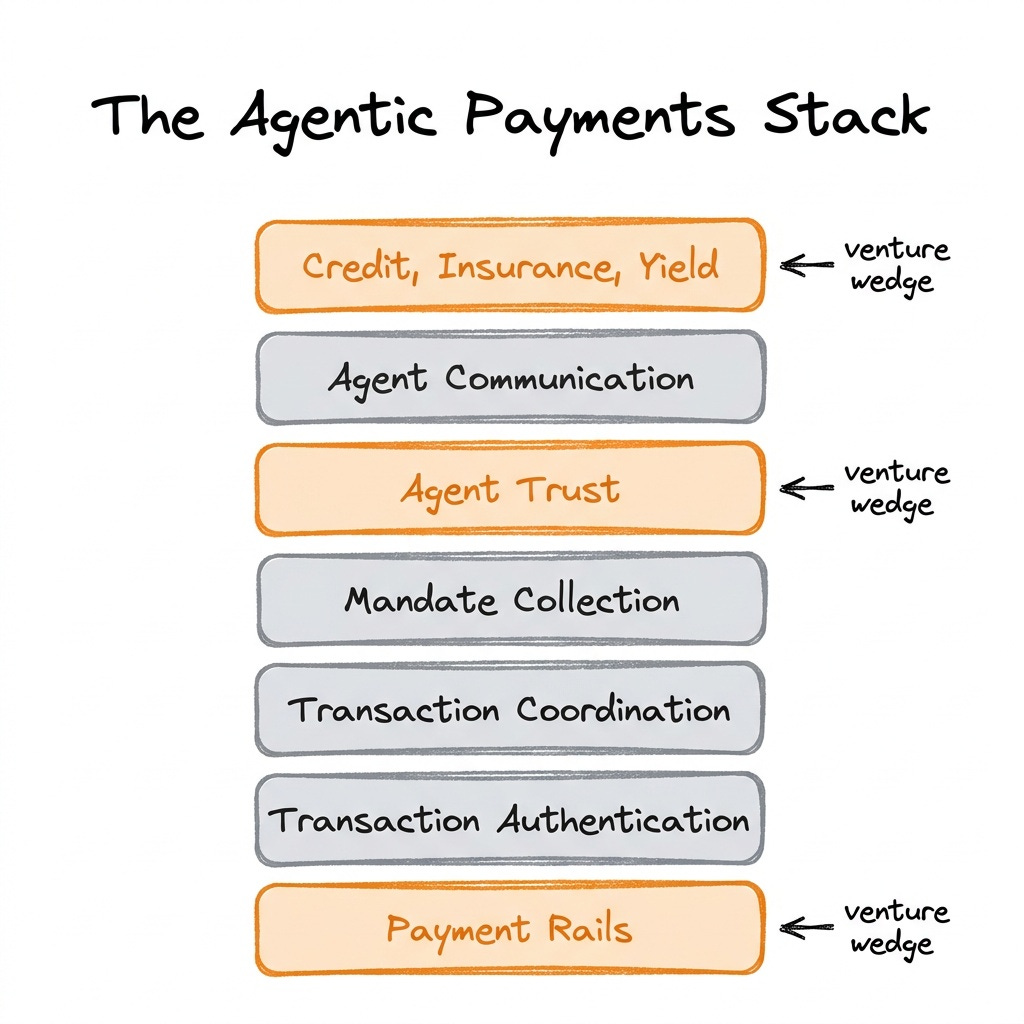

Agentic payments is not one problem. It is six:

How do agents talk to each other?

Should one agent believe another?

What is this agent authorized to do?

What is being bought?

Is the transaction legitimate?

How does the money actually move?

Most of the noise lives at the coordination layer, where OpenAI, Google, Visa, and Mastercard are racing to set the standard. That’s the layer where the platform players already own distribution.

Anyone building agentic checkout or agent wallet startups in that lane is filling a gap that Stripe Link CLI fills overnight. The product looks right today. It has no moat. The first time Stripe decides to compete in your category, the company is dead.

The wedges that matter for venture sit above and below the coordination layer.

The first is stablecoin-native rails purpose-built for agents. Coinbase’s x402 protocol moved $3M in its first seven days, after eighteen months of moving $80K. Whoever wins this category will build for agents directly, not for humans using agents.

The second is trust and identity for agents. The hard question is whether the agent on the other side of a transaction is real, has a track record, and will pay. The standards are still being written. ERC-8004 is the leading candidate: an Ethereum standard for on-chain agent identity and reputation, jointly authored by MetaMask, Google, Coinbase, and the Ethereum Foundation. Visa’s Trusted Agent Protocol is a centralized alternative.

But standards are not products. The companies that score agent reputation, verify what agents claim about themselves, and price agent risk for merchants and lenders do not exist yet. That is the opportunity. Whoever builds the credit bureau for software wins a category that did not exist three years ago.

The third is what sits on top of payments. Payment processing itself is a low-margin business. The money is in credit, insurance, FX hedging, and yield on the payment flows that the processing creates. Our portfolio company Rain proves this in stablecoin-backed cards: payments are the entry point, credit and rewards are the business. Agentic payments will follow the same pattern. The companies worth backing are not the ones fighting for payment processing market share. They are the ones building credit and insurance products for agents.

The honest counterpoint is that most agent builders today do not hold stablecoins. They have credit cards. So the path of least resistance for the next twelve months runs through Visa and Mastercard. That is true, and it is also why most of the early agentic payment startups will be acquired or killed by Stripe before they have a chance to build a moat. The companies that survive are the ones building on stablecoin rails today, accumulating users, reputation, and credit data, so that when the market shifts, they are already entrenched.

Another mistake the fintech crowd is making: real adoption in payments starts with a killer app. The app creates demand, and the demand drags infrastructure into existence. Stripe scaled because Shopify and Uber needed payment processing. Without them, Stripe is just another API. The agentic killer app has not arrived yet, and most agentic payment startups are building infrastructure ahead of the demand that would justify them. That is survivable. You wait for the app to show up, and you are ready.

But most of these startups are also building on credit card rails. That is not survivable. If the killer agentic app shows up on stablecoins, you cannot swap your foundation. You die.

So the bet is: stablecoin-native rails for agents. Trust and reputation infrastructure where crypto already has the lead. Credit and insurance products on top of agent payment flows. We are backing those companies. The rest of fintech is betting on the wrong rails.